.svg)

Investors showed little sign of following the adage, 'sell in May and go away…' last month as global equity markets continued to rally, brushing aside the economic fallout from the stalemate in the conflict between the US and Iran. Volatility remained elevated as the fragile ceasefire held for most of the month. Although missile exchanges briefly resumed towards the end of May, the month ended on hopes that both sides were close to agreeing a 60-day extension to the ceasefire leading to a reopening of the Strait of Hormuz.

Political turbulence in the UK has added to domestic investor uncertainty following Labour’s dismal performance in the local elections in early May. The Conservatives also suffered heavy losses, highlighting a more fragmented political landscape and the erosion of two-party dominance. Keir Starmer’s position as Prime Minister appears increasingly precarious, with Andy Burnham now widely seen as the frontrunner to succeed him. If Burnham wins the Makerfield by-election on 18th June a successful leadership challenge appears likely over the summer.

More important from a global investment perspective, was the meeting between Presidents Trump and Xi of China during the middle of the month. Whilst the meeting didn’t see any major deals announced it did provide some hopes of more stable ties between the two superpowers.

Central bankers remain paralysed by the uncertainty of the US Iran conflict. In the US Kevin Warsh was anointed as the new Governor of the Federal Reserve during the month and he faces a tricky balancing act to defy Trump wishes for lower interest rates against a backdrop of inflationary pressures driven by the high energy prices. The latest US PCE inflation reading showed a year-on-year increase to 3.8% and financial markets are currently betting that US rates will be higher by the end of 2026.

Bank of England Governor Andrew Bailey has signalled that they are not in a rush to increase rates despite a short-term inflation spike, with sluggish UK economic growth seen as more of a concern. In Europe, where rates are lower (2%) there is prospect of a hike in June with ECB policymakers split and Bank of Japan may also choose to hike rates next month if the energy shock persists.

So, despite the geopolitical headwinds, slowing growth and potential tightening of monetary policies across the globe, why do investors remain in bullish mood? Investment in AI is the key reason as the huge spending cycle is far reaching across countries and sectors. Companies are still spending and corporate earnings are supportive. But we appear to be in a self-fulfilling momentum driven rally – put simply the market is going up because people are buying it. Why are they buying it? Because it's going up! The question is how long fundamentals can support such exuberance.

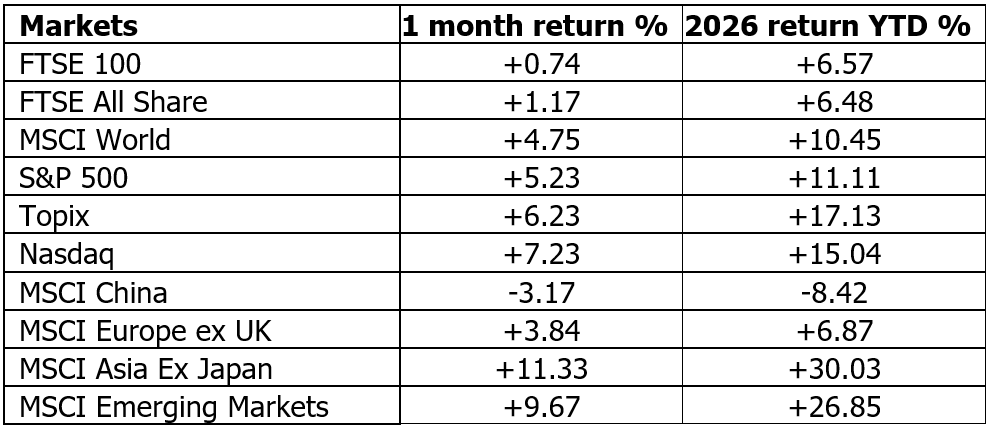

Stockmarkets across the globe remained firmly in risk-on mode in May. Optimism of a resolution to the conflict helped support markets that are focused on riding the AI driven wave. The MSCI World index posted a gain of 4.7% and US technology stocks remain at the forefront of the rally. The S&P 500 rallied 5.2% and tech heavy NASDAQ showed a monthly gain of 7.2% with both indices hitting new peaks near the end of the month. Nvidia beat market expectations for quarterly sales and profits (although the market didn’t seem that impressed) and is now valued at more than $5 trillion!

However, in May it was Asian and Emerging Markets that saw some of the strongest returns with the AI fuelled semi-conductor Supercycle leading to huge gains for South Korean and Taiwanese chip makers, resulting in the MSCI Asia Ex Japan index gaining 11.3% in May and a gain of 9.7% in the MSCI Emerging Markets index. The Japanese market also had a strong month, with the Topix up 6.2%.

European benchmarks also saw a strong boost with the MSCI Europe ex UK index up 3.8% but The UK stockmarket returns were more modest with the FTSE All Share gaining 1.2% in May not having a large tech presence to join in on the AI fuelled party and domestic political turbulence acting as headwinds.

In contrast to buoyant stockmarkets, bond markets have remained volatile in May as they continue to be spooked by inflationary pressures leading to a higher for longer interest rate environment. In the US, yields continued to climb and the ten-year treasury now pays 4.44% after offering 4.37% a month ago. In the UK increased political uncertainty has done little to support demand for gilts and the ten-year gilt hit a multi-decade of 5.17% at one point in May although by the end of the month receding concerns of rate increases saw it finish May at 4.85% down from 5.01% at the beginning of the month. In Japan, the ten-year JGB continued to rise from 2.52% to 2.65 with a rate rise in June priced in.

Turning to commodities and oil continues to be the key barometer for global markets and the price tumbled last month with May seeing the biggest monthly oil price drop since Covid, a clear signal of the optimistic view that a truce will be reached to imminently open the strait of Hormuz. May started with a barrel of Brent crude oil costing $110 and ended the month at $92.

Hopes for some form of resolution to the Middle East conflict also pushed gold lower during the month, while a stronger dollar and the prospect of higher interest rates weighed on demand. Gold ended May at $4,541 an ounce, down from $4,629 at the end of April.

In currency markets, the dollar rallied on expectations that US rates are staying higher for longer; rising 0.85% against the pound. The Euro was also stronger (by 0.36%) versus the pound on increased expectations of an ECB rate rise, but the Japanese Yen remains under pressure finishing 0.85% down in May versus sterling.

Monthly performance figures 30/4/26 to 30/5/26 source FE Analytics. N.b. the fund sectors exclude money market funds, markets are in local currency, and investment trusts exclude VCTs.

Important Information

This document is produced by Fairview Investing Ltd, an independent research consultancy in conjunction with James Scott-Hopkins. The content is for information purposes only and does not constitute financial advice. The commentary or research provided do not constitute a personal recommendation to deal. Any statements, opinions, forecasts, and figures are made by Fairview Investing (unless otherwise stated). They are considered to be reliable at the time of writing but may be subject to change.

Fairview Investing accepts no legal responsibility or liability for the content of this material. The contents of the document are not to be re-produced or circulated without the express permission of Fairview Investing Ltd. Fairview are independent investment consultants sitting on the Investment Committee of EXE Capital Management.

EXE Capital Management is a trading style of Everys Financial Services Ltd., an investment firm authorised and regulated by the Financial Conduct Authority, Firm Reference Number 998644.

Registered Office & Correspondence Address: 3 Priory Court, Priory Estate, Poulton, Cirencester, Gloucestershire, GL7 5JB.

Registered Company Number 14819837. VAT 459 9391 29.

+44 (0)1285 283 800

enquiries@execapman.com

Privacy Policy