.svg)

It feels like we have to start this month’s commentary with the budget (although you are probably sick of it by now). It will be most remembered for a farcical turn of events whereby the Office for Budget (ir)Responsibility inadvertently released details of the budget before the Chancellor stood up to speak! As widely expected, Rachel Reeves announced a series of tax hikes to the value of £26 billion to try and plug the gap (yawning chasm) in public finances. According to Schroders, the budget ‘has done enough to put UK public finances back on a sustainable path’ which may see the Bank of England cut interest rates before the end of the year.

But the ‘spend now pay later’ (Klarna budget!) is unlikely to stimulate the sluggish growth of the UK economy and the latest GDP figure for the third quarter was a Scrooge-like 0.1% following on from 0.7% in Q1 and 0.3% in Q2. The OBR forecasts for growth were reduced with GDP set to grow by 1.5% in 2025, 0.3% lower than projections in March, due to “lower underlying productivity growth". Unemployment has also hit the highest level since the Covid pandemic at 5%, however, slowing pay growth will cheer the Bank of England. Although rates remained unchanged last month at 4% Governor Bailey hinted they could cut soon as UK inflation eased somewhat in the last month to 3.6% from 3.8%.

Over the pond and the contrast is stark with the economy remaining robust, (but the longest shutdown in US government history that only ended last month has muddied the water over economic data releases). However, signs of a weakening in the labour market means that by the end of the month traders were betting on a further 0.25% rate cut by the Fed in December.

Interest rates remained steady in Europe and Japan in November. However, it is fiscal stimulus rather than monetary policy that is making headlines in Japan. At the end of the month Prime Minister Takaichi's government finalised a budget that contained a massive $135 billion debt financed stimulus package to help boost growth.

AI remains at the forefront of investors minds and Nvidia hit the news again last month. Good quarterly results cheered the market (initially) with revenue up 62%. However, not everyone is convinced; Japanese tech giant Softbank offloaded their entire $5.8 billion stake and Michael Burry (famous Big Short investor who called the credit crisis) has placed a $1.1 billion short against AI stocks including Nvidia. The spending merry-go-round between the tech giants continued with OpenAi signing a $38 billion deal with Amazon – how many times is the same dollar being spent and accounted for? It is perhaps no surprise that there was some profit taking in the AI leaders in November.

Turning to stockmarkets first and the concerns over high valuations of AI focused tech stocks saw a sell off during November with over $1 trillion wiped off the value of the major AI players during the month and the Tech focused Nasdaq falling 2%. However, despite more speculative areas selling off most developed markets recovered and the MSCI World index finished up 0.25%.

With only December to navigate 2025 is looking an excellent year for equity investors. Markets are up strongly with almost all areas in profit. Despite the uninspiring domestic economic outlook the UK market is holding its own with the FTSE 100 up 0.4% in November and 23% year to date. Back in January most investors were bearish on the outlook for China, but Hong Kong’s Hang Seng currently leads the pack with a rise of 33% so far this year despite being flat last month.

Lots going on in the bond markets last month with the UK government borrowing £9.9 billion more in the fiscal year. The ten-year gilt fell back marginally over the month having started November with a yield of 4.41% and finished paying 4.44%. The equivalent ten-year US treasury offered 4.08% a month ago and pays 4.01% now with hopes of a December rate cut providing support. Japanese Govt Bond yields increased last month in response to announcements of the debt financed fiscal stimulus package and the Bank of Japan hinted at more rate hikes, with a 10-year JGB now paying 1.81%.

Turning to commodities and gold has regained some of the shine lost in October. An ounce of gold was up 6% having started the month at $3996 and finished at $4254. Silver appears to be the metal to watch with it rising from just below $48 to finish at $56.5 – a five year high.

Oil had a poor month with the price of a barrel of Brent falling from $64.77 to finish at $62.38. With President Trump seemingly forcing a peace deal on Ukraine and Russia is there a glut of oil coming to the market soon? The price of a therm of natural gas also fell, possibly due to due Ukraine, with the price falling from 80.81 pence at the start of the month to end at 75.2 pence.

Finally, in currency markets Sterling had a good month overall despite or maybe because of the budget, although increased expectations of US rate cuts probably responsible for the pound gaining 0.75% versus the dollar. The pound rallied 2.1% versus the Yen and was flat versus the Euro.

For those who have been suffering FOMO from missing out on crypto gains this year, November highlighted the speculative risk as the price of Bitcoin plunged 18% (in dollars). Bitcoin does seem to provide a good barometer of risk and a sign that risk aversion is increasing.

Funds produced some interesting returns last month with gold and precious metals funds back to the foreground after a quiet October. Ninety One’s Global Gold fund topped the charts with a return of 14.5% with six further gold and precious metals funds in the top ten. The other key theme was healthcare and biotech after a spate of M&A this autumn. Candriam Oncology, admittedly fairly specialist, was only a whisker away from the top spot after rising 14.3%. Indeed the all-round strong showing helped propel the IA Healthcare sector to the top of the sector tables in November with a gain of just over 7%. Obviously, gold doesn’t have a sector otherwise that would probably have taken top spot. There is nothing in the top ten apart from precious metals and healthcare in November, in fact JPM Emerging Europe was the first other fund in the tables gaining 7.8% (in 20th place).

At the foot of the tables the higher growth funds dominated on the back of Nasdaq and AI related volatility. Growth stalwarts like Morgan Stanley US Growth featured which fell 10.7% - MS had three funds in the bottom ten. However, the wooden spoon in November went to Invesco Global Consumer Trends which fell 12.6%.

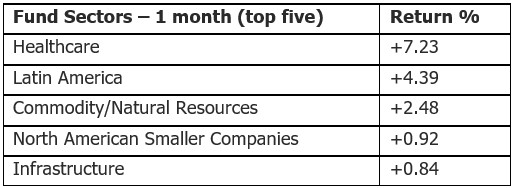

From an open-ended fund sector perspective, the aforementioned Healthcare sector topped the tables gaining 7.2% with Latin America a distant second with a rise of 4.4%. Tech was the worst performer last month falling 5.7% not helped by sterling rising against the US dollar.

Looking at investment trusts and in investment trust news, two of the big beasts in the infrastructure world announced a merger to create a £5.3 billion giant. However, the proposed deal between HICL and TRIG hasn’t gone down that well with investors and interestingly in a stock exchange announcement at time of writing the deal was called off. Biotech and healthcare was the dominant theme again with two trusts featuring in the top five and more in the top ten. The Biotech & Healthcare sector was the best performing sector in November with a gain of 7.3%.

Back to the budget, and whilst deeply unpopular with the voting public, reaction from fund managers was more subdued and best summarised by the feeling that “it could have been worse” after months of speculation and policy U-turns has been causing negative sentiment on UK assets. In bond markets Vanguard welcomed the certainty provided by the budget (according to FT) believing it will help bring gilt yields down. From an equity perspective Janus Henderson believe getting the Budget out of the way removes much of the uncertainty faced by UK businesses and consumers, allowing investors to focus on corporate fundamentals as opposed to political noise.

Globally, the latest Bank of America fund manager survey highlights a remarkable level of bullishness despite the exceptional tech driven returns this year. The latest survey highlighted that the most crowded trade continues to be a focus on the Magnificent 7 US Technology mega caps (overtaking gold as the most favoured trade). But at the same time a bubble in AI stocks is seen as the biggest risk with 45% of those surveyed citing it as a concern. This increasing nervousness may be the reason why there has been an increase in favour for more defensive areas such as healthcare and consumer staples as well as bonds.

Important Information

This document is produced by Fairview Investing Ltd, an independent research consultancy. The content is for information purposes only and does not constitute financial advice. The commentary or research provided do not constitute a personal recommendation to deal. Any statements, opinions, forecasts, and figures are made by Fairview Investing (unless otherwise stated). They are considered to be reliable at the time of writing but may be subject to change.

Fairview Investing accepts no legal responsibility or liability for the content of this material. The contents of the document are not to be re-produced or circulated without the express permission of Fairview Investing Ltd. Fairview are independent investment consultants sitting on the Investment Committee of EXE Capital Management.

EXE Capital Management is a trading style of Everys Financial Services Ltd., an investment firm authorised and regulated by the Financial Conduct Authority, Firm Reference Number 998644.

Registered Office & Correspondence Address: 3 Priory Court, Priory Estate, Poulton, Cirencester, Gloucestershire, GL7 5JB.

Registered Company Number 14819837. VAT 459 9391 29.

+44 (0)1285 283 800

enquiries@execapman.com

Privacy Policy