.svg)

2025 had started with many predicting that Trump’s stringent tariff policies would lead to the end of US economic exceptionalism. However, this has so far proved far from the mark and the year ended with the latest GDP reading show the US economy growing at a remarkable 4.3% in the third quarter, the strongest quarterly reading since 2023 and far exceeding analyst expectations. Whilst US consumer sentiment remains muted, growth is being driven by capital spending linked to AI investment.

At the same time the latest CPI reading showed US inflation moderating to 2.7% much lower than analyst forecasts. This provided breathing room for the Federal Reserve to cede to Trump’s demands and cut interest rates by 0.25% at their December meeting. As we go into 2026, an overheating of the US economy may be of more concern than a hard landing, especially given Trump has stated his intention to appoint a new Fed Reserve Governor "who believes in lower interest rates by a lot".

Closer to home and there is little chance of the UK and European economies overheating. Eurozone GDP grew by 0.2% in Q3, beating forecasts and proving more resilient than expected despite the tariff uncertainty. The ECB held interest rates at 2% in December.

The UK economic backdrop continues to paint a gloomy picture. GDP growth was revised down for the second quarter of 2025 to 0.2%. However, UK inflation fell more than expected in the latest November reading (to 3.2%) which allowed the Bank of England to cut rates by 0.25% to 3.75% in December.

Turning to Asia and the Bank of Japan is moving interest rates in the opposite direction to other central banks and in December raised interest rates to 0.75% (the highest level since 1999) to try and combat sticky inflation. China continues to demonstrate resilience to Trump’s tariffs and registered a $1.1 trillion trade surplus in physical goods for the first 11 months of 2025, compared to $1 trillion for 2024.

Going into 2026 economic fundamentals remain supportive with fiscal stimulus and lower interest rates supporting asset prices. However, after a stellar year for risk assets there are signs of irrational exuberance in certain areas. The Bank for International Settlements was the latest institution to sound a warning in its quarterly report stating that gold and US equities are showing the hallmarks of a bubble. Diversify, and proceed with caution seems like sound advice for the year ahead.

December saw most global stockmarkets extend their gains to make 2025 a remarkable year for equity investors. The MSCI World Index was up by 0.53% over the month which resulted in an annual gain of 18.4% (more than twice the long-term average return for equities). However, in sterling terms the return is reduced to 12.75%.

Despite the domestic economic malaise, the UK stockmarket has been exceptional and the FTSE 100 rallied a further 2.2% last month to finish 2025 with a remarkable total return (including dividends) of 25.8%. Defence stocks, financials and miners were some of the biggest winners.

The US stockmarket was flat in December and didn’t extend its global dominance in 2025. However, the S&P 500 still posted a return of 17% (although the effect of the weakening dollar significantly diluted annual returns for UK investors to 9.3% in sterling terms). Whilst technology has been a key long term driver of the US market it has not been all about the Magnificent 7 with five of them underperforming the wider US market, though the Nasdaq delivered a total return of 22.3% or 14.02% in sterling.

Alongside the UK, the strong recovery in Chinese stocks illustrated that 2025 was a good year to be a contrarian investor. The MSCI China index was marginally lower in December but gained 30% over the year despite lacklustre economic news from mainland China. The performance of China was a driver for MSCI Asia ex Japan and MSCI Emerging Markets benchmarks which both showed annual returns in excess of 31%. Latin America markets had a strong year boosted by demand for commodities and a weak US dollar, but India was a notable laggard as investors remained concerned over high valuations.

Looking at the bond markets and despite pre-Christmas rate cuts from the US Fed and Bank of England, both US and UK ten-year bonds ended December offering a higher yield than a month earlier. The ten-year gilt ended the year offering 4.48% having started December paying 4.44% while the ten-year US Treasury finished with a yield of 4.17% compared to 4.01% a month ago. Over the year bonds treaded water again despite rate cuts with coupon clipping plus a tiny capital return the norm.

Turning to commodities and gold hit another new all-time high in December before finishing the year at $4331, a remarkable rise of 62% in 2023 as investors sought refuge from dollar weakness, geopolitical uncertainty and ongoing inflationary pressures. Silver has had an even more remarkable year playing the catch-up game with an ounce costing $71 now compared to $56 at the start of December and showing a rise of 144% for the year. Oil had another poor month with the price of a barrel of Brent falling from $62.38 to finish at $60.85. well below the price at the start of 2025 when Brent traded at $74 a barrel; there appears to be no end to the weakness with over supply a key issue.

Finally, in currency markets Sterling had a good month gaining against euro, dollar, and yen. Over the year the picture was more mixed though: sterling gained 6.92% against US dollar, 6.65% versus the yen but fell 5.5% against the Euro. The US dollar lost ground against all three currencies in 2025. In dollar terms, Bitcoin fell 7.99% last year – one risk asset that didn’t perform well in 2025!

Turning to funds now and the December was a microcosm of 2025. Precious metals and commodity funds dominated the month and the year on the back of historic gold and silver price rises. Seven of the top ten funds in December were commodity related and the entire top ten best performing funds last year were gold, commodity and precious metals funds with Baker Steel Gold & Precious Metals taking top spot with an annual gain of 184%.

At the foot of the tables last month the only loose theme was healthcare – three health related funds featured in the bottom ten in December. Over the calendar year one area stood out for mediocre performance, India. Six of the bottom ten funds in 2025 were Indian and Invesco India Equity was the Wolves of the fund world propping up the table with the fund falling 17%. There were a number of suspended property funds delivering poor returns last year, but many of these are winding up which distorts the performance figures therefore they were excluded.

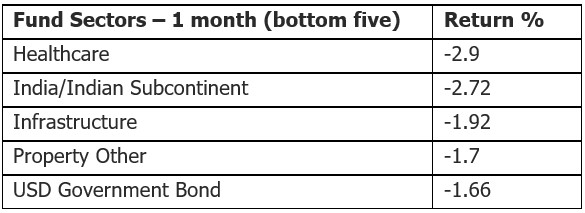

Looking at the IA fund sectors now and December saw the Financials sector take top spot. 2025 threw up a slight surprise as the top performer was Latin America – the commodity boom and a weak US dollar helped the average Latam fund gain 38% last year. The Commodity & Natural Resource sector finished second in 2025 with a rise of 29.7%. Propping the fund sector tables last month was Healthcare (falling 2.9%) but over the course of last year, the Indian sector was the only sector to post a negative return with the average fund falling 9%. Three US sectors featured in the bottom five in 2025 not helped by a weak US dollar.

Over to investment trusts now and 2025 was a year of M&A and takeovers with some sharp share price rises for takeover targets, especially in the infrastructure and renewables area. However again it was commodity trusts that dominated with the AIC Commodity & Natural Resources sector gaining 61% in 2025. Golden Prospect Precious Metals was the top performing trust last year rising 164%. The Latin America sector came second with a gain of 51%. Interestingly the Property Logistics sector finished third last year gaining just over 50% fueled by consolidation and takeovers in the sector – property has been so unloved that it feels as if a snapback could be a theme to watch in 2026.

Investors have been handsomely rewarded for taking on risk in 2025 and the latest Bank of America fund manager survey shows professional investors being at their most bullish since 2021. Such euphoria sounds a warning signal for the contrarian, and the survey also indicates that cash levels held by portfolio managers has fallen to just 3.3% its lowest level on record. In terms of what may derail the rally in 2026, survey respondents see the AI bubble bursting or a private credit-related crash as the biggest tail risks for global markets.

The end of 2025 was notable for marking Warren Buffett’s last day at the helm of Berkshire Hathaway – if you had invested $100 with Mr Buffett when he took the helm at Berkshire it would be worth a measly $5.5 million today. Will there be another CEO/investor like him and has he shrewdly timed his exit given where market valuations are?

Monthly performance figures 30/11/25 to 31/12/25 and YTD 31/12/24 to 31/12/25 source FE Analytics.

Important Information

This document is produced by Fairview Investing Ltd, an independent research consultancy. The content is for information purposes only and does not constitute financial advice. The commentary or research provided do not constitute a personal recommendation to deal. Any statements, opinions, forecasts, and figures are made by Fairview Investing (unless otherwise stated). They are considered to be reliable at the time of writing but may be subject to change.

Fairview Investing accepts no legal responsibility or liability for the content of this material. The contents of the document are not to be re-produced or circulated without the express permission of Fairview Investing Ltd. Fairview are independent investment consultants sitting on the Investment Committee of EXE Capital Management.

EXE Capital Management is a trading style of Everys Financial Services Ltd., an investment firm authorised and regulated by the Financial Conduct Authority, Firm Reference Number 998644.

Registered Office & Correspondence Address: 3 Priory Court, Priory Estate, Poulton, Cirencester, Gloucestershire, GL7 5JB.

Registered Company Number 14819837. VAT 459 9391 29.

+44 (0)1285 283 800

enquiries@execapman.com

Privacy Policy