.svg)

Investors remained remarkably calm in June, in the face of ongoing uncertainty over Trump’s tariff policies and an escalation of the Middle East conflict. Last month’s big story was the Israeli attack on Iran, which was followed by the US attack on Iranian nuclear enrichment facilities. There is an uneasy truce currently, of course by the time this gets sent out that might be outdated! Whilst the oil price initially spiked, markets took the increased geopolitical risk in their stride. Do market participants think the Iranian threat has gone or that in the event of a financial wobble central bankers will ride to the rescue with monetary stimulus.

As has been the case since last November we probably should start with President Trump and his latest pronouncements. Whether his strategies are correct or not is questionable, but he is making an impact. Iran’s nuclear deterrent may have been neutralised, whilst the 90-day deadline for countries to make trade deals with the US will is imminent on 8th July. China is the country everyone is looking at and last week a deal was supposedly signed by the two countries though no one knows what’s in it. Clearly China has been the goal all along, not just from Trump, but also Joe Biden before him. The Europeans also seem happy, if latest reports are true, with the universal tariff proposals suggested by Trump but with some carve outs. Do the numbers matter or is it certainty that markets crave?

Trump’s “big, beautiful tax bill” is making its way through Congress passing a Senate vote by a narrow majority at the weekend for them to fully debate it. His former friend, Elon Musk, isn’t a fan as in his view it will just pile on further debt to an almost $35 trillion debt pile.

Moving back home and chancellor Rachel Reeves has had a mixed bag of economic news recently. Whilst the UK was the fastest growing G7 economy in the first quarter of 2025, it only grew by 0.7%. The national insurance hike on businesses, has had a hit to the number of employees and lower pay hikes. The latter is probably welcome to dampen inflation, but the former will be a concern with unemployment now at a 4-year high. With UK inflation slowing slightly to 3.4% in May (it’s still well above target) GDP fell 0.3% in April – has the dreaded stagflation returned? The Bank of England maintained rates at 4.25% at their June meeting, but with a deteriorating economy surely further cuts are on the way.

Elsewhere and inflation looks marginally better with Euro area CPI falling below the ECB’s 2% target in May and they cut rates by another 0.25% to 2%. Jerome Powell at the Federal Reserve is taking a wait and see approach (much to the ire of Trump who is back on the “sack Powell” mantra which is worrying investors) the Fed thinks US inflation will accelerate to 3% in 2025 due to a one-off tariff shock before falling back next year.

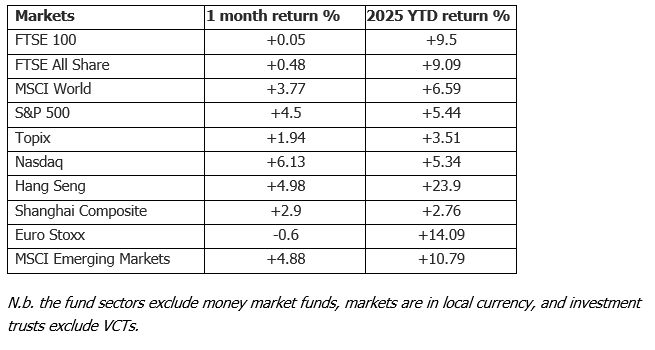

Risk assets remained in favour in June and the MSCI World index gained 3.8%, whilst the S&P 500 was up 4.5% for the month to end June at an all-time - astonishing really with the global backdrop, tariffs, wars, Deepseek, and high valuations. Tech returned to favour with the Nasdaq up over 6% in June and the US titans are still driving markets ever upwards. There doesn’t seem to be any end to the obsession with AI – it was reported last month that Elon Musk’s xAI has raised a further $9.3bn in funding valuing the business at $80 billion. Whilst the likes of Nvidia and Microsoft throw off cash to be invested into AI development. Will the AI gold rush come to a juddering halt at some point? The FTSE was flat was a raft of average data left investors unexcited and a weak dollar weighed on blue chip earnings. with 75% of FTSE 100 earnings coming from outside the UK.

The story in the first half of 2025 is generally good for stockmarket investors. The surprising winner year to date has been Hong Kong’s Hang Seng index gaining 23.9%. Europe has also been a surprise with the Eurostoxx gaining 14.1%. The FTSE 100 produced a creditable 9.5% in six months, not to be sniffed at. The interesting one is the US where despite a fresh record high for the S&P 500, the year-to-date gain of 5.4% has been more than wiped out by currency losses for UK investors.

Falling interest rates are good for bond markets given the inverse relationship between bond yields and bond prices. 2025 has been the year of rate cuts with 64 cuts globally so far – this is the highest figure since 2020. On the back of recent news the US ten-year treasury finished June offering a yield of 4.23% down from 4.4% a month ago. The UK ten-year gilt had a similar move after starting June offering 4.65% and closing the month with a yield of 4.49%. Germany’s ten-year bond rose 0.1% to finish at 2.6% and the equivalent JGB fell marginally and now yields 1.43%.

Turning to commodities now and an ounce of gold was flat on the month, starting at $3315 and finishing at $3307. Gold has now overtaken the Euro as the world’s second largest reserve asset after the US dollar with 20% of central bank reserves now shiny. The price of a barrel of Brent crude was more volatile, spiking sharply during Israel’s attacks on Iran. Over the month the price of a barrel of Brent rose just under $4 to close at $67.61 however intra month the price almost hit $80.

In foreign exchange markets the dollar slumping has been the key theme and is trading at levels versus the pound last seen in 2021. A stronger pound is good for inflation as we import so many goods but bad for UK earnings. The same is true but magnified in Japan where a strong Yen normally equals a weak stock market. Year to date, the dollar has lost 13.7% against the Euro, 9.6% versus the pound and 9.1% against the Yen, significantly diluting returns for overseas investors long of the US markets.

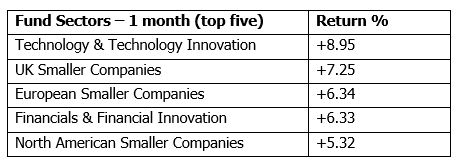

Looking at funds now and Barings Korea fund topped the tables with a gain of 19.34% (on the back of Korean election results and on hopes of an imminent US rate cut that tends to lift all of Asia and emerging markets). Elsewhere in June’s top ten technology funds were the major theme with stalwarts such as Polar Global Technology making the top ten. From a fund sector perspective IA Technology was first in June with the sector gaining an average of 6.35%. The Global Emerging Markets sector was a slightly surprising second place gaining 3.68% then again if the US China trade deal is about to be signed and the dollar remains weak then the outlook for EM is positive. Slightly randomly the UK Index Linked Gilt sector had a good month too finishing third.

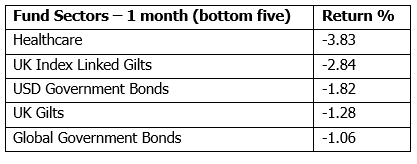

At the foot of the tables last month was a cohort of US bond sectors not helped by the pound gaining 1.82% versus the dollar in June. In fact, the three US bond sectors at the foot of the tables were the only ones to deliver a negative return. USD Government Bond sector propped the tables falling 0.39%.

Turning to trusts now and takeovers, corporate actions, and strategic reviews were yet again the story of June – and the universe continues to shrink with takeouts (Downing Renewables) and mergers (Henderson EuroTrust with Fidelity European). At least in the case of Downing the agreed takeover price was above the listing price of a few years ago and in the meantime, investors have had many dividends. SDCL Efficiency Income trust topped the tables in June with a gain of 31% - however the big caveat is the share price is still only 56 pence whilst it was over 120p a few years back. In fact, Downing aside the top five last month were all trusts massively down on IPO prices and in the case of Digital 9 it is 90% down – maybe it should be renamed as Down 90.

From a trust sector perspective Capital Growth topped the tables with a gain of 7.91% closely followed by the Renewable Energy Infrastructure sector.

Briefly over six months the weak dollar has helped push the Latin America sector to the top of the fund tables with a gain of 17.78% - the bull run in some commodities has probably helped too. Elsewhere the story is all Europe with three European sectors in the top five of the IA universe with the banker of UK Equity Income completing the top five with a gain of 9.11%. Whereas the foot of the tables is dominated by US Smaller Companies – not helped by a weak dollar impacting UK investors.

The Bank of America Global Fund Manager Survey can often prove a contrarian indicator, so it is perhaps a little concerning that the latest survey shows a jump in sentiment among professional investors. The June survey showed that fund managers are moving out of defensive strategies and taking on more risk in their portfolios on hopes of a soft landing for the global economy. In a recent meeting with Multi Asset fund manager Keith Balmer at CT he believes that despite significant geopolitical driven volatility nothing changed fundamentally in the global economy and expects markets to revert to focusing on growth inflation and interest rate movements in the second half of the year. Whilst he does not believe that will be a significant growth shock from Trump’s tariff policies, he did sound caution that in the short-term it feels like complacency setting in given high market valuations and geopolitical risk, so volatility may increase over the summer.

Important Information

This document is produced by Fairview Investing Ltd, an independent research consultancy. The content is for information purposes only and does not constitute financial advice. The commentary or research provided do not constitute a personal recommendation to deal. Any statements, opinions, forecasts, and figures are made by Fairview Investing (unless otherwise stated). They are considered to be reliable at the time of writing but may be subject to change.

Fairview Investing accepts no legal responsibility or liability for the content of this material. The contents of the document are not to be re-produced or circulated without the express permission of Fairview Investing Ltd. Fairview are independent investment consultants sitting on the Investment Committee of EXE Capital Management.

EXE Capital Management is a trading style of Everys Financial Services Ltd., an investment firm authorised and regulated by the Financial Conduct Authority, Firm Reference Number 998644.

Registered Office & Correspondence Address: 3 Priory Court, Priory Estate, Poulton, Cirencester, Gloucestershire, GL7 5JB.

Registered Company Number 14819837. VAT 459 9391 29.

+44 (0)1285 283 800

enquiries@execapman.com

Privacy Policy