.svg)

Tariffs continued to dominate global headlines in July, with investors focused on President Trump's game of "deal or no deal". Yet investor sentiment has remained sanguine with the much talked about TACO trade (a premise that Trump Always Chickens Out) allaying fears that we will not see the stringent level of tariffs that would result in the global economy grinding to a halt. However, Trump has been getting deals done and Europe conceded to 15% tariffs on imports from EU and it appears that US/China will extend their trade truce with President Xi having invited Trump to meet in the coming weeks – potentially allowing him to announce another “great deal”.

Whilst investors worst fears may have been allayed, from the beginning of August US consumers will be paying at least 15% on imported goods (levels not seen since the 1930s) and time will tell how this will affect demand and inflation in the World’s largest economy. The US economy so far appears resilient, with the latest reading showing 3% GDP for the second quarter although the figure was boosted by the sharp drop in imports. But US consumption (the key driver of growth) has slowed considerably this year and inflation remains above target, with the latest reading for PCE inflation at 2.8%. Against a mixed bag of economic data Fed Reserve Governor Jerome Powell resisted Trump’s demands for interest rate cuts at the July meeting – although there was dissent in ranks (the first time since 1993) as two members voted to cut rates.

It feels like a UK rate cut may be on the cards with the Labour Government’s plans to boost growth not materialising. The UK economy shrank by 0.1% in May and the IMF have put their oar in recommending the Bank of England should cut rates in August to boost demand, but the latest UK CPI of 3.6% is still well above the Bank’s target. In marginally better news, the IMF, upgraded the UK’s growth forecast for 2025 to 1.2% and 1.4% next year. Sir Keir will be hoping the UK deal with Donald Trump will pay off with UK’s tariffs (10%) lower than the EU.

In Europe it feels likes the ECB has reached the endgame for rate cuts for now – to be fair they’ve been arguably the most proactive in central banks and are maybe ahead of the curve – they paused rate cutting cycle last month whilst tariff negotiations were ongoing with President Trump. Time will tell how the tariff deal will affect Europe’s exporters – the deal did not please German politicians or business leaders.

Economic prospects in China are looking up despite tariff uncertainty. The economy grew at 5.2% in Q2 and in their latest report the IMF increased the 2025 growth forecast to 4.8% a significant upgrade on their previous forecast for 4.0%. The strength of the World’s second largest economy is illustrated by the commencement of the Mega dam project in Tibet which is due to cost over $160 billion!

Stockmarket investors are paying little heed to economic and political turbulence as they continue to ride the wave of the AI inspired tech boom. The MSCI World index was up 2% in July and the US S&P 500 hit new highs and finished the month up by 2.2% driven by mega cap tech stocks. Meta, Apple and Microsoft’s quarterly earnings helped keep the tech bandwagon rolling with Apple and Meta revenue beating expectations and increasing their commitment to spend on AI whilst Microsoft became the second company (after Nvidia) to hit $4 trillion market cap. To put this in context the market capitalization of the London Stockmarket is about $3.4 trillion.

The tech deficient FTSE also reached several all-time highs last month breaking through the 9000 level in the process and gaining 4.31% in July. China also had a good month with both Shanghai and Hong Kong rising over 4%.

On the back of a busy month for economic data bond yields were heading back up. The UK ten-year gilt rose marginally starting with a yield of 4.49% and finishing a 4.57%. The US ten-year treasury also rose and more than the UK finishing July offering 4.37% after starting with a yield if 4.23%. In Japan the equivalent JGB now pays 1.55% up from 1.43%.

Turning to commodities now and an ounce of gold was range bound for the second month in a row. The gold price started July at $3307 and finished at $3343 an ounce. Over the month the price of a barrel of Brent rose just under $5 to close at $72.53 – interestingly London listed oil majors released profits well down on the equivalent period in 2024. The biggest move in commodities came in the copper market – where the price fell back 20% at the end of the month when it was announced the metal would be exempt from tariffs!

On the forex markets last month, the pound gained marginally against the Yen but lost 0.72% versus the Euro and 3.73% against the US Dollar. In fact, the greenback was strong against all major currencies, recovering some of the ground lost in the first half of the year. For currency geeks the Big Mac Index has recently been updated and its bad news for the resurgent pound 2025. According to their global measure of the ubiquitous fast-food, sterling is overvalued by 13.5% versus the US dollar. The Swiss Franc remains the most expensive currency today with a 49% overvaluation.

Looking at funds and as well as the ongoing momentum of tech funds there were three more contrarian trends in the open-ended fund world in July: biotech, China, and clean energy. Two of those three were somewhat of a surprise as they’ve been in the doldrums for a while now. China was not a surprise as it’s had a strong 2025 overall with the Hang Seng leading the index pack by a large margin year to date. Biotech and solar/clean energy are interesting as they’ve been unloved and shunned for much of the last three years, in fact shunned since interest rates started rising post covid. All three of these themes last month could be considered cheap value plays and you could definitely include the resurgent UK FTSE 100 in that camp too! Pictet Biotech topped the chart with a gain of 13.4% followed closely by Active Solar with a rise of 13.4% - Active Solar was last seen in these pages with repeated appearances in the worst performing charts. Whilst Pictet Biotech was the only such fund in the top ten, there were many more biotech and health related funds in the top 30.

At the foot of the table there were also a few clear themes; UK smaller companies, and property. Since the lows of early April UK Small caps have risen over 18% so a pause for air is unsurprising. Church House UK Smaller Companies propped the tables with a fall of 4.9% - Castlefield Thoughtful UK Smaller Companies also featured at the bottom. By the way, what has happened with fund groups abandoning simple fund names and adding daft adjectives – it isn’t going to make the fund more marketable.

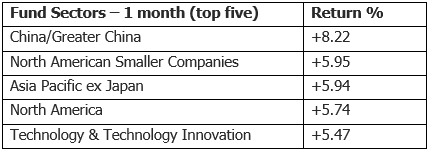

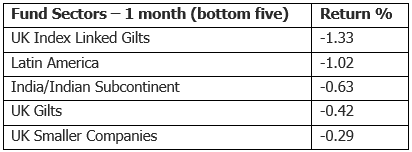

From a fund sector perspective China gained most with the average fund rising 8.2%. Chinese gains also helped drag the Asia Pacific ex Japan sector into the top five too. The two US sectors also featured partially on the back of the strong rise in the dollar versus sterling which clearly helped UK investors. Latin America and India were both in the bottom five last month – possibly no surprise as the likes of Mexico and Brazil are yet to come to a deal with Trump over tariffs and India looks like it will be hit with a rate of 25%. However, UK Index Linked Gilts propped the table with a fall of 1.3% in July.

Looking at investment trusts briefly and there was the usual mixed bag in the top five in July. Manchester & London gained an impressive 16% but does have 60% invested in just two stocks: Nvidia ad Microsoft. Diversification isn’t the name of the game for this trust. Biotech Growth Trust also made the top five also gaining over 16% however top spot went to Apax Global which rose 31%. China trusts topped the sector tables with a gain of 10% with more specialist sectors such as Leasing and Infrastructure Securities also making the top spots.

Trying to make sense of the effect of tariffs on corporate profits is the number one dilemma for fund managers at the current time, but the latest Bank of America fund manager survey continues to indicate consensus bullish sentiment. Only 31% of fund managers polled this month are predicting a weaker global economy in the coming months – this compares to 82% of managers polled in April – are investors getting a little complacent?

The pressure exerted by Donald Trump on the Federal Reserve ratcheted up in July and a lack of independence of the US Central Bank would be a concern for bond managers. Dan Ivascyn the CIO at Bond gurus PIMCO was very clear that any attempt to reduce independence of the Federal Reserve “would be very bad for markets”.

N.b. the fund sectors exclude money market funds, markets are in local currency, and investment trusts exclude VCTs.

Important Information

This document is produced by Fairview Investing Ltd, an independent research consultancy. The content is for information purposes only and does not constitute financial advice. The commentary or research provided do not constitute a personal recommendation to deal. Any statements, opinions, forecasts, and figures are made by Fairview Investing (unless otherwise stated). They are considered to be reliable at the time of writing but may be subject to change.

Fairview Investing accepts no legal responsibility or liability for the content of this material. The contents of the document are not to be re-produced or circulated without the express permission of Fairview Investing Ltd. Fairview are independent investment consultants sitting on the Investment Committee of EXE Capital Management.

EXE Capital Management is a trading style of Everys Financial Services Ltd., an investment firm authorised and regulated by the Financial Conduct Authority, Firm Reference Number 998644.

Registered Office & Correspondence Address: 3 Priory Court, Priory Estate, Poulton, Cirencester, Gloucestershire, GL7 5JB.

Registered Company Number 14819837. VAT 459 9391 29.

+44 (0)1285 283 800

enquiries@execapman.com

Privacy Policy