.svg)

February ended in dramatic fashion, as the US and Israel launched “major combat operations” on Iran in the early hours of Saturday 28th February. Long term leader Ayatollah Khamenei has been killed as air strikes pounded Tehran, creating a power vacuum with the US urging the Iranian people to seize power. There has been a swift response from Iran, attacking US supporting states in the region and at this point it is unclear how the conflict escalates from here and what the humanitarian cost will be.

Viewing it from an investment perspective it is important stress that this is not a “black swan” event that might shock markets. Trump had telegraphed his intentions and when talks broke down on Iranian de-nuclearisation on Thursday the risk of conflict was high. The supply shock in the Gulf will likely cause oil prices to surge and in the short-term push investor sentiment into "risk-off" trades selling higher risk equities and favouring safe haven assets like Government bonds and gold.

Before the breakout of conflict, there were other reasons for investors to be more cautious in February. Trump doubled down on his aggressive approach to tariffs, imposing a rate of 15% following the Supreme court ruling that imposition of his original tariff policies was unlawful.

Investors are becoming increasingly nervous as to whether the rewards from AI will justify the eye watering amounts being spent by the US technology “hyperscalers”. February saw a sell off in mega cap US tech stocks who announced spending plans of $660 billion for the year according to the FT. At the same time new kid on the block, Anthropic, is highlighting the risk to incumbents making waves with competitive AI offerings.

US economic growth for the fourth quarter of 2025 came in well below expectations at an annualised rate of just 1.4%. At the same time US inflation came in at the highest level since March 2024 with the December PCI reading increasing to 2.9%. This reduces the probability of imminent US interest rate cuts, especially if the Middle East conflict leads to a prolonged rise in oil prices.

News-flow in February seems to vindicate the investment theme that has been in play to diversify away from the US assets. The UK has been a beneficiary and despite Keir Starmer polling as the most unpopular Prime Minister (a high bar to hurdle) and a resounding defeat in the recent Gorton and Denton by-election, the political noise shouldn’t distract from an economy where the corporate sector is in strong financial shape and January saw some relief for the treasury with announcement of a record £30.4 billion budget surplus. Whilst UK rates were held last month, inflation fell to 3% increasing the odds of a rate cut in March (although Middle East uncertainty may defer the decision).

Another beneficiary of US divestment has been Japan where Sanae Takaichi scored a resounding victory in the General election. This was welcomed by investors in the Japanese stockmarket in response to her pursuit of “responsible yet aggressive fiscal policy”.

Whilst escalation of conflict in the Middle East ratchets up global investor uncertainty, trying to react to short-term geopolitical volatility is futile. The impact on fundamentals is likely to be minimal and the message is not to panic and maintain a long-term investment perspective.

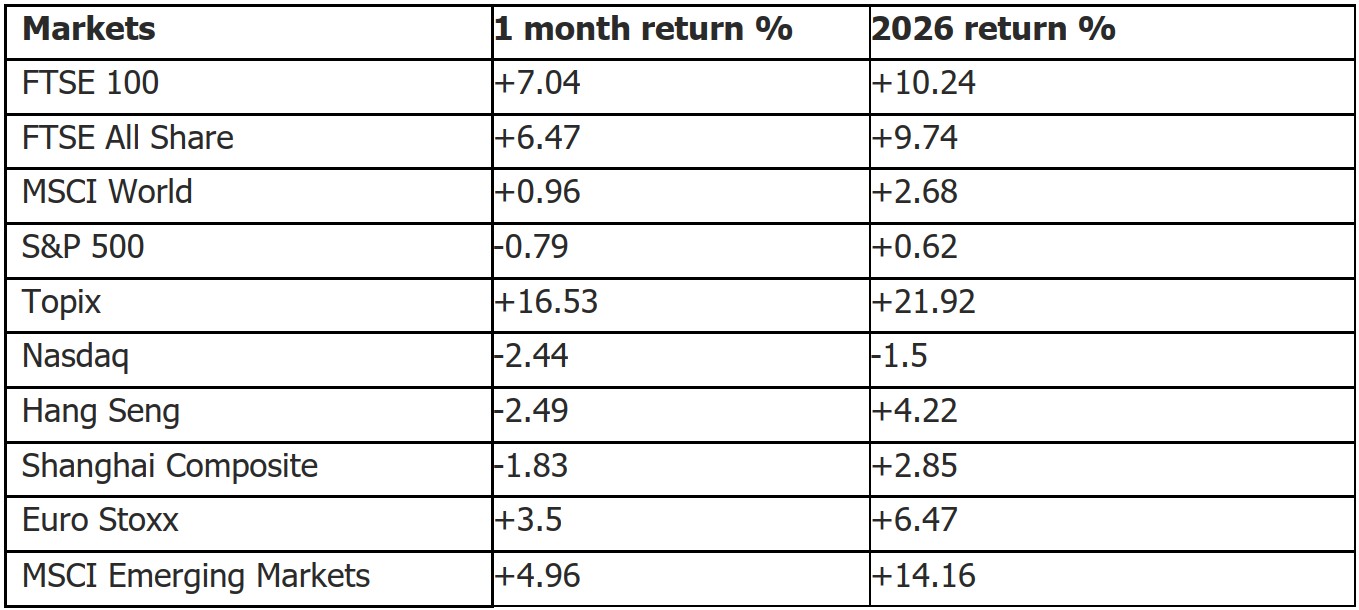

Starting with stockmarkets and whilst the global equity benchmark MSCI World index posted a 0.96% return in February this masked a significant disparity across style and geography. Nervousness over US tech mega caps AI spending saw the S&P 500 fall back by -0.8% whilst the Tech focused NASDAQ finished the month -2.4% lower. From a style perspective there was a clear favour for value versus growth with the MSCI World Value index up 3.2% and the MSCI World Growth index down 1.4%.

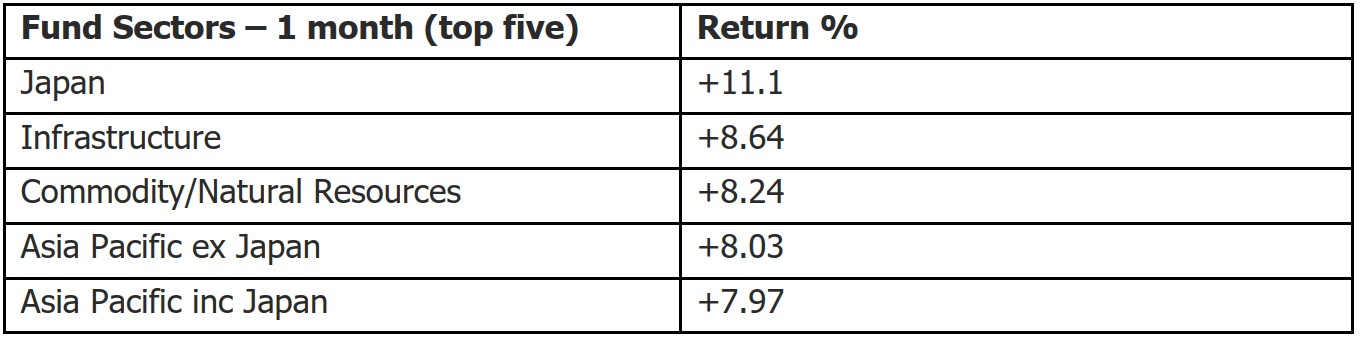

There was a stellar month for the Japanese stockmarket where the Topix gained a remarkable 16.5% on the back of the landslide election victory for PM Takaichi. But it was Korea that was the standout performer with the KOSPI up by 20.7% driven by AI Chipmakers Samsung and Hynix. The AI and commodities rally helped push the MSCI Asia Ex Japan index 5.4% and MSCI Emerging Market index up by 4.5% in February.

It was another good month for the UK with a new all-time high of 10,910 for the FTSE last week. The new high was driven by well received annual results from HSBC and the FTSE gained 7% in February and is up 10% so far in 2026.

Looking at the bond markets and it’s been a strong month for government bonds with prices rising and yields falling. The UK ten-year gilt started February offering 4.52% and now pays 4.23%. There was a similar move across the Atlantic with the ten-year Treasury dipping back below the 4% level; a month ago the yield was 4.24% and it closed on Friday at 3.94%. Even the ten-year JGB rallied despite the likelihood of more fiscal stimulus from the now very powerful PM Takaichi – the yield is now 2.11% compared to 2.24% at the end of January. With the Middle East conflict pushing investors into Risk-off mode it would not be a surprise to see further near-term gains for bond markets.

In commodity markets all eyes are on the oil price. February saw a hardening of the price and a barrel of Brent ended at a month high of $72.87 after starting the month costing $70.69. It will be interesting to see what happens after the US attack on Iran; the likelihood is a short-term spike, but maybe lower prices long term. The gold rollercoaster continues. A plunge in prices at the backend of January didn’t herald the start of further downward spiral, in fact it was a recent low point. During February the price of an ounce of gold steadily regained lost ground and finished the month up over 10% at $5247 an ounce. Silver regained a little ground after the historic falls in January and for context is almost three times the price of a year ago; currently $93.78.

In currency markets the pound had a weak month on expectations of lower rates falling 1.3% against Yen, 0.8% Euro and almost 2% versus the US dollar. But year to date it’s still up versus the dollar and only marginally lower against Yen and Euro. Will the attack on Iran see the dollar to strengthen?

A persistent theme when meeting fund managers since the advent of Trumponomics 2.0 has been dollar weakness. The greenback saw some respite in February (and in the short-term may strengthen in a flight to haven assets if the Middle East conflict escalates). But consensus amongst investment strategists we speak to is that a weakening dollar is a long-term structural theme. JPMorgan strategists believe that the appointment of a Dovish Chair of the Federal Reserve may lead to further weakening, whist a recent meeting with a Fidelity economist illustrated their belief is that we are in a multi-year downward cycle for the dollar. Predicting currencies is notoriously difficult, but for those holding significant exposure to US assets having some hedged exposure feels like it may be prudent.

Monthly performance figures 31/1/26 to 28/2/26 source FE Analytics. N.b. the fund sectors exclude money market funds, markets are in local currency, and investment trusts exclude VCTs.

Important Information

This document is produced by Fairview Investing Ltd, an independent research consultancy. The content is for information purposes only and does not constitute financial advice. The commentary or research provided do not constitute a personal recommendation to deal. Any statements, opinions, forecasts, and figures are made by Fairview Investing (unless otherwise stated). They are considered to be reliable at the time of writing but may be subject to change.

Fairview Investing accepts no legal responsibility or liability for the content of this material. The contents of the document are not to be re-produced or circulated without the express permission of Fairview Investing Ltd. Fairview are independent investment consultants sitting on the Investment Committee of EXE Capital Management.

EXE Capital Management is a trading style of Everys Financial Services Ltd., an investment firm authorised and regulated by the Financial Conduct Authority, Firm Reference Number 998644.

Registered Office & Correspondence Address: 3 Priory Court, Priory Estate, Poulton, Cirencester, Gloucestershire, GL7 5JB.

Registered Company Number 14819837. VAT 459 9391 29.

+44 (0)1285 283 800

enquiries@execapman.com

Privacy Policy